Steel's 2026 Double Squeeze: CBAM Goes Live and the Safeguard Gets Tougher

Steel importers buying into the EU and exporters shipping to EU buyers are navigating two major regulatory changes at once in 2026 - and the timing is not a coincidence. The EU's Carbon Border Adjustment Mechanism (CBAM) entered its financially binding definitive phase on 1 January 2026. Six months later, on 1 July 2026, a new and significantly tougher steel safeguard regime replaces the existing one. Together, they reshape the landed cost of every tonne of imported steel in ways that go well beyond a routine tariff adjustment.

This post explains both mechanisms, how they interact, and what you should be doing about each of them right now.

Part 1: CBAM - From Reporting to Paying

What changed on 1 January 2026

For the previous three years, CBAM was a reporting exercise. EU importers of steel, aluminium, cement, fertilisers, electricity and hydrogen had to submit quarterly reports on the embedded emissions in their imports - but no money changed hands. That phase ended on 31 December 2025.

From 1 January 2026, CBAM entered its definitive phase, transforming what was a reporting-only obligation into a financially binding compliance regime. The shift is fundamental: EU importers (or their indirect customs representatives) who bring more than 50 tonnes of in-scope goods into the EU per year must now hold authorised CBAM declarant status, report embedded emissions annually, and - from 2027 - purchase and surrender CBAM certificates priced at the EU ETS carbon price.

Iron and steel are core covered sectors. The first annual declaration, covering all 2026 imports, is due by 30 September 2027. Certificate sales open on 1 February 2027. The financial exposure, however, accrues from every shipment made in 2026 onwards.

The CBAM factor: small now, large later

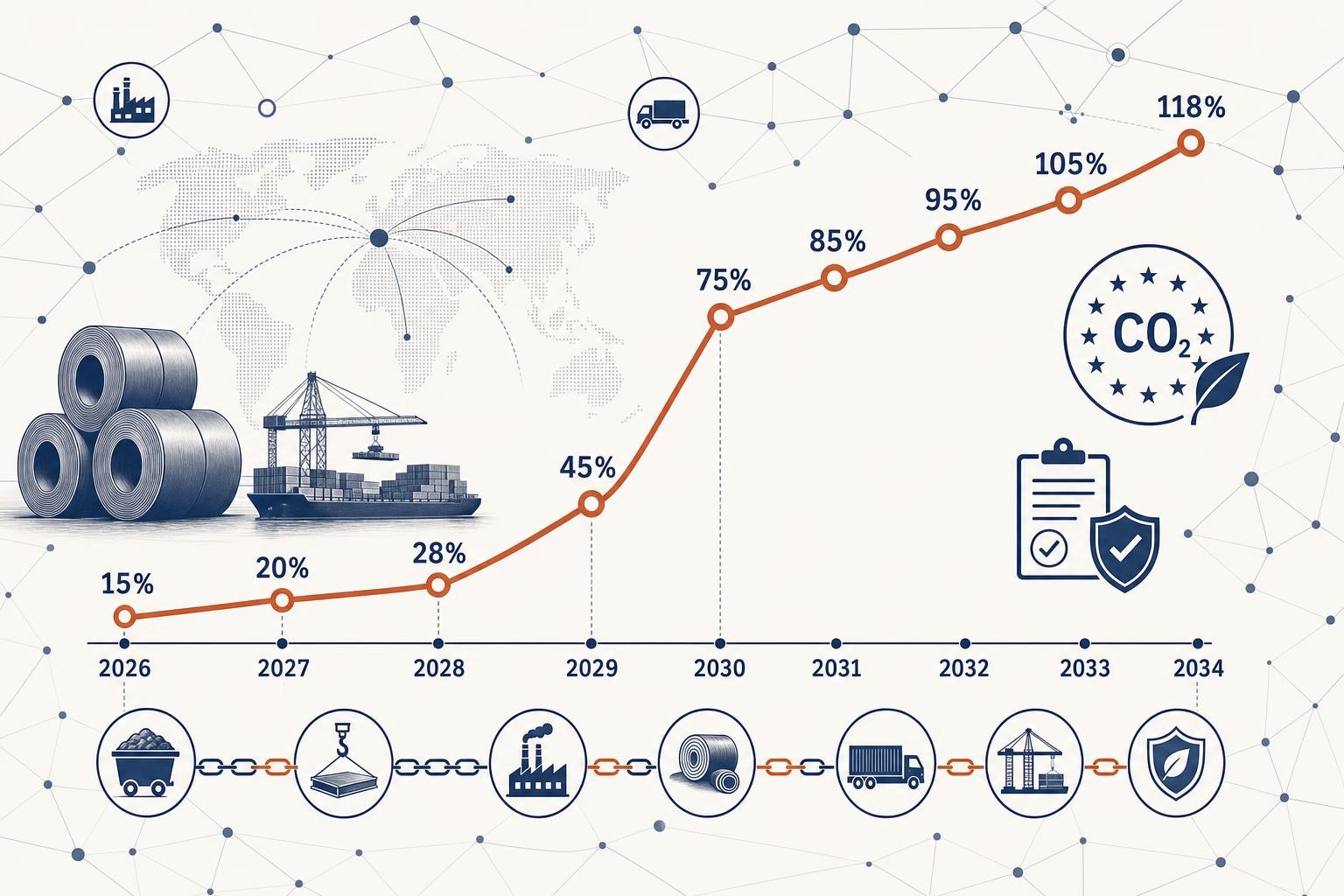

CBAM does not immediately charge for 100% of embedded emissions. It uses a CBAM factor that mirrors the phase-out of free ETS allowances given to EU steelmakers. In 2026, the CBAM factor is 2.5%, rising to 5% in 2027 and accelerating from there, reaching 100% by 2034.

The formula is straightforward:

CBAM cost = tonnes × embedded emissions (tCO₂/t) × ETS price (€/tCO₂) × CBAM factor

At the Q1 2026 certificate price of €75.36 per tonne CO₂ and a 2.5% factor, a 500-tonne shipment of blast-furnace steel with embedded emissions of 2.0 tCO₂/t generates a CBAM cost of approximately €1,884 for that quarter. That sounds manageable. But by 2030, with the factor approaching 50% and ETS prices potentially higher, the same shipment could cost ten times as much.

Why steel's emissions profile matters so much

The production route is the single most important cost variable for steel importers under CBAM.

Blast furnace-basic oxygen furnace (BF-BOF) steel carries an embedded emissions factor of approximately 2.0 tCO₂ per tonne, generating a gross certificate cost of approximately €150 per tonne at €75/tCO₂. Electric arc furnace (EAF) steel, produced primarily from recycled scrap, carries approximately 0.5 tCO₂ per tonne - a gross cost of around €37.50 per tonne at the same price. That is a four-to-one difference in gross CBAM exposure, purely based on how the steel was made.

Only direct (Scope 1) emissions are priced for steel - electricity consumed in production is excluded. This matters for EAF producers, whose main emissions are process-related rather than from power consumption.

Default values: the hidden cost trap

If a mill cannot provide verified actual emissions data, the EU applies default values set conservatively above typical actual performance. Default values carry a mark-up of 10% in 2026, rising to 20% in 2027 and 30% from 2028 onwards. For steel, the gap between actual and default can be enormous: one market source described Indian HRC default costs at over €200 per tonne, making previously attractive import offers suddenly uneconomic.

The practical implication: EU importers who rely on default values for their 2026 declaration will pay more than necessary, and the mark-up compounds over time. Getting verified actual emissions data from your mills is not a nice-to-have - it is a direct cost-reduction lever.

The 2026 CBAM factor is 2.5% — but the data you collect now locks in your cost base for 2027 and beyond. Importers who secure verified actual emissions from their mills in 2026 will have a significant cost advantage as the factor ramps toward 100% by 2034. Importers relying on default values face rising mark-ups (10% → 30%) on top of an already conservative baseline.

Part 2: The New Steel Safeguard - Tighter Quotas, Higher Penalties

What the Commission proposed - and what was agreed

The existing EU steel safeguard, in place since 2018, expires on 30 June 2026. It cannot be renewed under WTO rules. On 7 October 2025, the European Commission proposed a replacement regulation (COM(2025) 726). After intensive negotiations, the European Parliament and Council reached a provisional agreement on 13 April 2026, with the new regime set to enter into force on 1 July 2026.

The headline numbers are stark:

The new system reduces overall EU steel import quotas by approximately 47% compared to 2024 safeguard quotas, setting total annual tariff-free import volumes at 18.3 million tonnes, and doubles the out-of-quota duty from 25% to 50%.

| Feature | Current safeguard (to 30 Jun 2026) | New regime (from 1 Jul 2026) |

|---|---|---|

| Annual tariff-free quota | ~33 million tonnes | 18.3 million tonnes (−47%) |

| Out-of-quota duty | 25% | 50% |

| Product categories | 26–28 | 30 |

| Quarterly carry-over | Allowed | Year 1: allowed; Year 2+: Commission review |

| Origin rule | Customs origin | Melt and pour (from 1 Oct 2026) |

| Duration | Expires 30 Jun 2026 | From 1 Jul 2026; review within 6–12 months |

The 50% out-of-quota duty applies in addition to any other duties already in force - including anti-dumping duties where applicable. This is not a marginal adjustment. Importers should expect significantly more shipments to fall outside quota limits, triggering the higher rate.

The "melt and pour" rule: a new origin test

One of the most consequential innovations in the new regime is the melt and pour requirement. From 1 October 2026, importers must provide evidence - typically a mill certificate - identifying the country where the steel was originally melted and poured: the location where raw steel and iron was first produced in liquid form in a steelmaking furnace.

This matters because the current safeguard uses standard customs origin, which can be the country of last substantial transformation. Under melt and pour, steel that was melted in China but re-rolled in Vietnam is counted against China's quota allocation - not Vietnam's.

The rule directly affects countries that rely on imported slabs or hot-rolled coil for re-rolling and finishing. Countries such as Turkey, Vietnam, Thailand and Malaysia, which have significant downstream processing capacity but limited or no crude steel production, may find their effective quota access reduced as the melt-and-pour origin is traced back to the original producing country.

Within two years, the Commission must assess whether melt and pour should become the formal basis for country-specific quota allocations. As one legal analysis put it, this shift may be a matter of "when" rather than "if."

Who is most affected - and who benefits

The stainless steel segment illustrates the trade-flow impact most clearly. Exports from South Korea and Taiwan are set to be the most affected, with out-of-quota cold-rolled coil (CRC) volumes representing approximately 7% and 10% of their respective 2026 CRC production. Asia accounts for over 70% of stainless steel imports into the EU, led by South Korea and Taiwan.

On the other side of the ledger, some origins are likely to benefit from safeguard exemptions. Countries such as Algeria, Brazil, Indonesia and Saudi Arabia - which contribute a small share of EU import volumes - are expected to retain or gain exemptions under developing-nation provisions, allowing their steel to enter the EU tariff-free. Ukraine has historically received special consideration given its exceptional security situation, and the Commission has indicated candidate countries in that position will be given particular treatment when quotas are set.

Safeguard exemptions are product-category specific. A country that is exempt for hot-rolled coil may not be exempt for cold-rolled or coated products. Always check the specific category (1–30) for your CN codes, not just the headline country status.

Part 3: How CBAM and the Safeguard Interact

The two mechanisms are legally separate - CBAM is a carbon pricing instrument; the safeguard is a trade defence measure - but they compound each other in practice.

S&P Global noted that European market participants say the combination of CBAM costs and stricter safeguards "removes the safety valve of cheap third-country supply that previously capped European prices." The result is a higher, regulation-driven price floor for flat products, even without a demand-led recovery.

One analysis estimated that without trade adjustments, EU steel importers could face combined added costs of around 37% - approximately €5.9 billion in safeguard tariff costs on volumes exceeding the new quotas, plus approximately €3.8 billion in CBAM costs on embedded emissions (assuming 2024 carbon prices and a fully phased-in CBAM factor).

The interaction also creates a carbon-origin dimension that did not exist before. An importer sourcing from a safeguard-exempt origin with lower embedded emissions - say, EAF-produced steel from a country with a recognised domestic carbon price - could simultaneously avoid the 50% out-of-quota duty and reduce their CBAM certificate obligation. That is a meaningful competitive advantage as the CBAM factor ramps up.

Part 4: What to Do Now

If you are an EU importer of steel

If you import more than 50 tonnes of steel (or other CBAM goods) per year, you must hold authorised CBAM declarant status. Applications submitted by 31 March 2026 allow provisional continued importing while the National Competent Authority processes your application. If you have not yet applied, do so immediately.

For each supplier and CN code, check: (a) which safeguard quota category applies and whether your origin has a country-specific allocation or falls under the residual 'other countries' bucket; (b) whether your origin is safeguard-exempt; and (c) what the CBAM embedded emissions profile looks like for that mill and production route.

Default values carry a 10% mark-up in 2026 (rising to 30%) and are set conservatively high. For blast-furnace steel, the gap between actual and default can be hundreds of euros per tonne at full CBAM factor. Ask your suppliers for installation-level emissions data calculated using EU-prescribed methodologies, and ensure it is verified by an accredited third party.

For each key supply lane, model two scenarios: in-quota (duty-free + CBAM cost) and out-of-quota (50% duty + CBAM cost). The financial gap between the two is substantial. Update these models quarterly as TRQ utilisation data becomes available from the Commission.

From 1 October 2026, you must be able to provide evidence of the country of melt and pour at importation. Embed documentary-evidence clauses in your supply contracts now, and request mill certificates from suppliers that identify the original melting location.

As the CBAM factor ramps toward 100% by 2034, the production route of your steel becomes a major cost driver. EAF-produced steel from mills with verified low emissions carries a fraction of the CBAM cost of blast-furnace steel. Factor this into medium-term sourcing strategy.

If you are a non-EU steel exporter

Your EU customers are now under real financial pressure from CBAM, and they will pass that pressure to you in the form of data requests and pricing negotiations. Here is what you need to do:

- Provide installation-level emissions data. EU importers cannot use actual values in their CBAM declarations unless the data is verified by an EU-accredited third-party verifier. Engage a verifier for your 2026 production year now - the first verification includes an on-site audit.

- Understand your melt-and-pour origin. If your facility re-rolls or processes steel from imported slabs or HRC, identify where that input material was originally melted and poured. This will determine how your exports are counted against quota allocations from 1 October 2026.

- Know your safeguard quota category. Check which of the 30 product categories your exports fall into, and whether your country has a country-specific allocation, falls under the residual quota, or is exempt. Country allocations will be set by the Commission through implementing acts.

- Provide CBAM communication data proactively. EU importers need your embedded emissions data in a format compatible with the CBAM Registry. Providing this promptly - and accurately - is a commercial differentiator. Importers are already shifting toward suppliers who can deliver clean, verified data.

The Bigger Picture

The 2026 double squeeze is not a temporary disruption. The CBAM factor ramps steadily to 100% by 2034, and the new safeguard regime includes a review mechanism that could tighten further. The Commission is also proposing to extend CBAM to approximately 180 downstream steel and aluminium products from January 2028, which would bring finished goods such as car parts and appliances into scope.

The structural direction is clear: the EU is pricing carbon into imported steel while simultaneously restricting the volume of tariff-free imports. For importers, the combination rewards lower-carbon sourcing from origins with good quota access. For exporters, it rewards investment in emissions measurement, verification infrastructure, and - over the medium term - lower-carbon production routes.

The companies that treat 2026 as a preparation year for a much tighter 2027-2034 environment will be better positioned than those managing each deadline in isolation.

Related reading

CBAM Cost Trajectory: Why 2026 Is Cheap and 2030 Will Hurt

CBAM looks affordable in 2026 - but the cost escalates nearly 40x by 2034. Here's the full phase-in schedule, the 2029-2030 cliff edge, and how to budget now.

CBAM Penalties and Enforcement: What EU Importers Need to Know

A clear guide to CBAM penalties under the definitive regime - the €100/tonne rule, unauthorised-import sanctions, how member states enforce, and how to stay on the right side of the rules.

CBAM Certificate Lifecycle: Buying, Holding, and Surrendering - A Cash-Flow Guide for Importers

A plain-English guide to the CBAM certificate lifecycle - when to buy, the 50% quarterly holding rule, the 30 September surrender deadline, and how to plan your cash flow around EU ETS pricing.