CBAM Cost Trajectory: Why 2026 Is Cheap and 2030 Will Hurt

Your first CBAM bill will feel manageable. That's by design - and it's also a trap for finance teams who stop there.

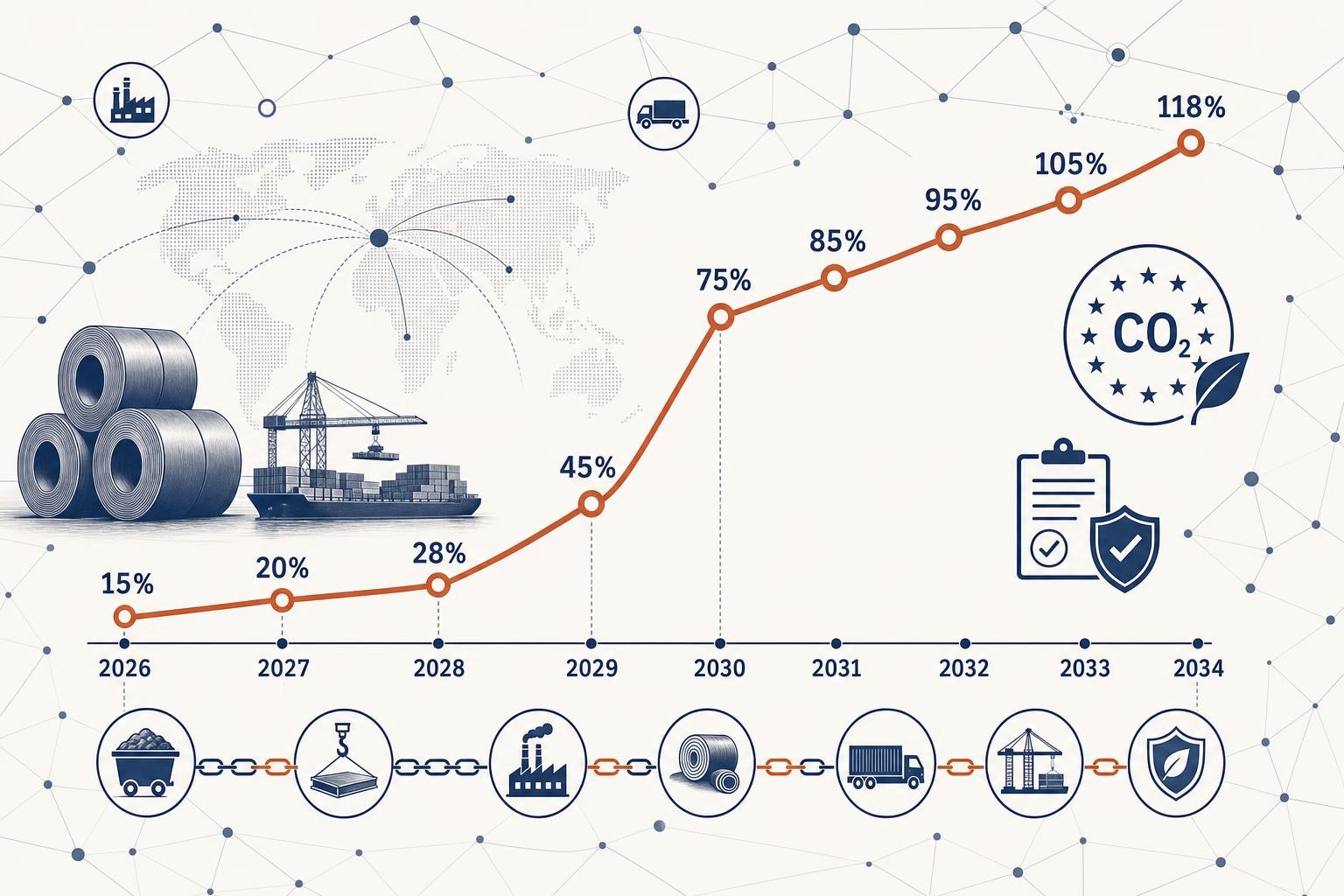

The CBAM factor in 2026 is just 2.5%. For every tonne of steel you import, you're only paying the carbon price on a tiny slice of its embedded emissions. The regulation is deliberately gentle at the start. But the factor doesn't stay gentle. It ratchets upward every year through 2034, when it hits 100% and the full carbon cost lands on every tonne you import.

The net certificate cost at full phase-out in 2034 is roughly 40 times larger than the first-year obligation in 2026 for the same import volume. If your procurement team is modelling CBAM as a line item based on today's number, they're planning for the wrong decade.

This post is about the cost curve - what it looks like year by year, where the dangerous jump is, and how to build a budget that doesn't get blindsided.

Why the Cost Is Low Now: The Free Allocation Link

CBAM doesn't exist in isolation. It's the mirror image of a parallel process happening inside the EU Emissions Trading System (EU ETS): the phase-out of free allowances for domestic EU producers in CBAM-covered sectors.

As long as EU domestic producers receive EU ETS allowances at no charge, the EU carbon border adjustment mechanism applies only to the fraction of emissions that are no longer covered by free allocation. The CBAM factor in any given year equals the percentage by which free allocation has been reduced.

In other words: the CBAM factor is low in 2026 because EU steelmakers, cement producers, and aluminium smelters still receive most of their ETS allowances for free. As those free allowances are withdrawn, the CBAM factor rises in lockstep. Industrial activities covered by CBAM will receive a free allocation which will gradually decrease to zero from 2026 to 2034 and will be replaced step-by-step by the CBAM.

This is the mechanism that makes the cost trajectory so steep in the second half of the decade.

The Phase-In Schedule: Year by Year

The CBAM factor rises from 2.5% in 2026 to 100% in 2034, following a fixed schedule set in the regulation. Here is the complete picture:

The rate of reduction of free allocation - and therefore the CBAM factor - is as follows: 2026: 2.5%; 2027: 5%; 2028: 10%; 2029: 22.5%; 2030: 48.5%; 2031: 61%; 2032: 73.5%; 2033: 86%; 2034: 100%.

Notice the shape of that curve. The first three years (2026-2028) are a gentle slope. Then the gradient steepens sharply. The steepest single-year jump occurs between 2029 and 2030, when the factor increases from 22.5% to 48.5%. That's more than a doubling in a single calendar year.

The 2029–2030 cliff edge. The CBAM factor more than doubles between 2029 (22.5%) and 2030 (48.5%) — the largest single-year jump in the entire phase-in schedule. Any importer who hasn't modelled costs beyond 2028 will face a budget shock in 2030. Start planning for it now.

A Worked Example: Blast-Furnace Steel

Numbers make this concrete. Take a mid-market importer bringing in blast-furnace steel - the most common form of primary steel - from a non-EU supplier.

The baseline inputs:

- Embedded emissions: ~2.0 tonnes CO₂ per tonne of steel (typical for blast-furnace/basic oxygen furnace production)

- CBAM certificate price: ~€75 per tonne CO₂ (the Q1 2026 price was set at €75.36)

- Gross CBAM cost at full phase-in: 2.0 × €75 = €150 per tonne of steel

Because 97.5% of free ETS allocation for CBAM sectors remains in 2026 (CBAM factor: 2.5%), the effective certificate obligation is only 2.5% of gross embedded emissions. A blast furnace steel importer paying approximately €75 per tonne CO₂, with an emission factor of approximately 2.0 tonnes CO₂ per tonne of steel, faces a gross CBAM cost of approximately €150 per tonne but a net 2026 obligation of approximately €3.75 per tonne, because of this allocation offset.

Here's how that same tonne of steel scales across the decade, holding the carbon price constant at €75:

| Year | CBAM Factor | Net Cost (€/tonne steel) | Multiple of 2026 cost |

|---|---|---|---|

| 2026 | 2.5% | €3.75 | 1× |

| 2027 | 5% | €7.50 | 2× |

| 2028 | 10% | €15.00 | 4× |

| 2029 | 22.5% | €33.75 | 9× |

| 2030 | 48.5% | €72.75 | 19.4× |

| 2031 | 61% | €91.50 | 24.4× |

| 2032 | 73.5% | €110.25 | 29.4× |

| 2033 | 86% | €129.00 | 34.4× |

| 2034 | 100% | €150.00 | 40× |

Two things jump out. First, the 2030 cost (€72.75/t) is nearly 20 times the 2026 cost - and it arrives in a single step from 2029's €33.75. Second, by 2034, the CBAM cost per tonne of steel equals the entire gross carbon cost of the product. There is no more free-allocation cushion.

Important caveat on the carbon price: This table holds the ETS price flat at €75 for illustration. The actual price will move. Simple, transparent CBAM cost models based on EU ETS prices help you quantify exposure for key materials and steer procurement and decarbonisation decisions before costs escalate through 2034. For budgeting purposes, run at least three scenarios: a base case at current prices, a downside if ETS softens, and an upside toward €90-100.

What the Omnibus Simplification Changes (and Doesn't Change)

The 2025 Omnibus simplification (Regulation (EU) 2025/2083) adjusted several operational mechanics. It doesn't change the cost trajectory - the phase-in schedule is untouched - but it does affect cash flow timing and quarterly holding requirements.

Certificate sales start date. Sales of CBAM certificates via a centralised platform to authorised CBAM declarants, covering emissions embedded in goods imported in 2026, will start from 1 February 2027. This was postponed from the original 1 January 2026 start date. Certificates purchased in 2027 for 2026 imports will be priced using the quarterly average of 2026 EU ETS allowance prices. Thereafter, CBAM certificate prices will equal the weekly average of EU ETS auction closing prices.

Quarterly holding requirement. The requirement for declarants to hold a number of CBAM certificates on their registry account at the end of each quarter is reduced to 50% of embedded emissions in goods imported since the beginning of the calendar year (down from 80%). This eases the liquidity pressure of building up a certificate position through the year.

What hasn't changed. The CBAM factor schedule is fixed in the primary regulation. The 2029-2030 cliff is not going away. The Omnibus gave importers more time and a lighter quarterly burden - it did not reduce the ultimate cost.

Build Your CBAM Budget: Four Practical Steps

The cost trajectory is knowable. The uncertainty is the carbon price, not the factor schedule. Here's how to build a budget that holds up.

Use the factor schedule above to project your CBAM cost at current ETS prices for each year through 2030. This is the minimum planning horizon. The 2029–2030 jump is the single most important number in your model — flag it explicitly for finance and procurement.

The CBAM factor is fixed; the carbon price isn't. Build a base case (current €75/tCO₂), a downside (€55), and an upside (~€100). The factor ramp means that even a flat carbon price produces a rising CBAM bill every year — so the upside scenario in 2030 can be significant.

Default values carry a mark-up — 10% in 2026, 20% in 2027, and 30% from 2028 onwards for most sectors. Suppliers with verified lower-than-default emissions reduce your assessed tonnage and therefore your certificate obligation. The earlier you engage suppliers on this, the more budget headroom you create.

For 2026 imports, the certificate price is set retrospectively using the quarterly average ETS price for the quarter in which you imported — not the price on the day you buy certificates in 2027. Keep a record of your import dates by quarter so you can match them to the correct price when certificates go on sale in February 2027.

Default values cost more than they look. Using default values avoids the cost of supplier verification — but the 30% mark-up applied from 2028 onwards means you're paying for 130% of the default embedded emissions. For high-volume importers, the verification cost often pays for itself within a year or two of the 2028 mark-up kicking in. Run the numbers before assuming defaults are the cheaper path.

Use the CBAM Cost Calculator

The table above is a static illustration. Your actual exposure depends on your import volumes, your specific products, your suppliers' emission intensities, and any carbon price already paid in the country of origin.

The Bigger Picture: What This Means for Procurement

The cost trajectory has strategic implications that go beyond the finance team's spreadsheet.

Supplier selection will increasingly be a carbon decision. By 2030, a steel supplier with 1.5 tCO₂/t embedded emissions costs you meaningfully less in CBAM certificates than one at 2.5 tCO₂/t - at the same purchase price. The carbon intensity of your supply chain becomes a procurement variable, not just an ESG metric.

Pass-through conversations need to start now. If you're planning to pass CBAM costs to customers, the 2026 number is easy to absorb. The 2030 number is not. Contracts that don't include a CBAM escalation clause will create margin pressure as the factor ramps.

The downstream scope expansion is coming. The Commission has published a legislative proposal for an extension of the CBAM scope to an additional 180 aluminium- and steel-intensive downstream products, with implementation beginning on 1 January 2028. If you import fabricated steel or aluminium products that aren't currently in scope, that may change.

Key Dates to Put in Your Budget Calendar

| Date | What happens |

|---|---|

| 1 Jan 2026 | Definitive CBAM period begins; CBAM factor = 2.5% |

| 1 Feb 2027 | Certificate sales open; 2026 certificates go on sale |

| 30 Sep 2027 | First annual declaration and certificate surrender deadline (for 2026 imports) |

| 1 Jan 2028 | CBAM factor rises to 10%; default value mark-up increases to 20% |

| 1 Jan 2029 | CBAM factor rises to 22.5% |

| 1 Jan 2030 | CBAM factor jumps to 48.5% - the cliff edge |

| 1 Jan 2034 | Free allocation reaches zero; CBAM factor = 100% |

The official source for the definitive CBAM rules is the European Commission's CBAM page. The complete free allocation phase-out schedule is documented at cbamguide.com.

The Bottom Line

The CBAM factor rises from 2.5% in 2026 to 48.5% in 2030 - a near-doubling in a single year between 2029 and 2030. For a blast-furnace steel importer, that translates from a manageable ~€3.75/tonne today to ~€72.75/tonne in 2030, at the same carbon price.

The regulation is designed to be gentle at first and steep later. Finance teams that model only the 2026 number are planning for the easy years. The hard years - 2029, 2030, and beyond - are where the budget exposure becomes material.

Model the full curve now. Engage your suppliers on actual emissions data. Watch the 2029-2030 transition. And keep an eye on the ETS price, because the factor schedule is fixed but the carbon price is not.

Related reading

The Article 9 Deduction: How to Cut Your CBAM Certificate Bill with Carbon Prices Paid Abroad

Article 9 of Regulation (EU) 2023/956 lets you deduct a carbon price already paid in the country of origin from your CBAM certificate obligation. Here's exactly how it works - and how to claim it.

CBAM Record-Keeping and Audit Readiness: The Importer's Practical Guide

CBAM compliance isn't just about the 30 September declaration. Here's the practical guide to the data trail, four-year retention rules, and NCA audit readiness every authorised declarant needs.

CBAM and Imported Electricity: Why the Physical Hourly PPA Is Now the Only Route Off the Default

Electricity behaves differently under CBAM than any other covered sector. Here's exactly how the definitive regime works for cross-border power - and why only a physical hourly PPA can reduce your liability.