CBAM Certificate Lifecycle: Buying, Holding, and Surrendering - A Cash-Flow Guide for Importers

You already know your tonnes of embedded emissions. Now comes the part that hits the balance sheet: turning that number into certificates, holding the right amount at the right time, and surrendering them before the deadline. Get the mechanics wrong and you face a €100-per-tonne penalty - on top of still having to buy the certificates.

This guide walks through the full CBAM certificate lifecycle with a cash-flow lens, so your finance and treasury teams know exactly what to budget, when to buy, and how to avoid a painful September scramble.

The Certificate as Your "Payment" Instrument

A CBAM certificate is the unit of account for the whole system. One certificate equals one tonne of CO₂ equivalent of embedded emissions. As an authorised CBAM declarant, your job is to:

- Buy certificates from your national authority via the EU's centralised common platform.

- Hold a minimum number at the end of each quarter throughout the year.

- Surrender the full amount required for the prior year's imports by the annual deadline.

Everything else - the pricing formula, the quarterly rule, the surrender date - flows from those three steps.

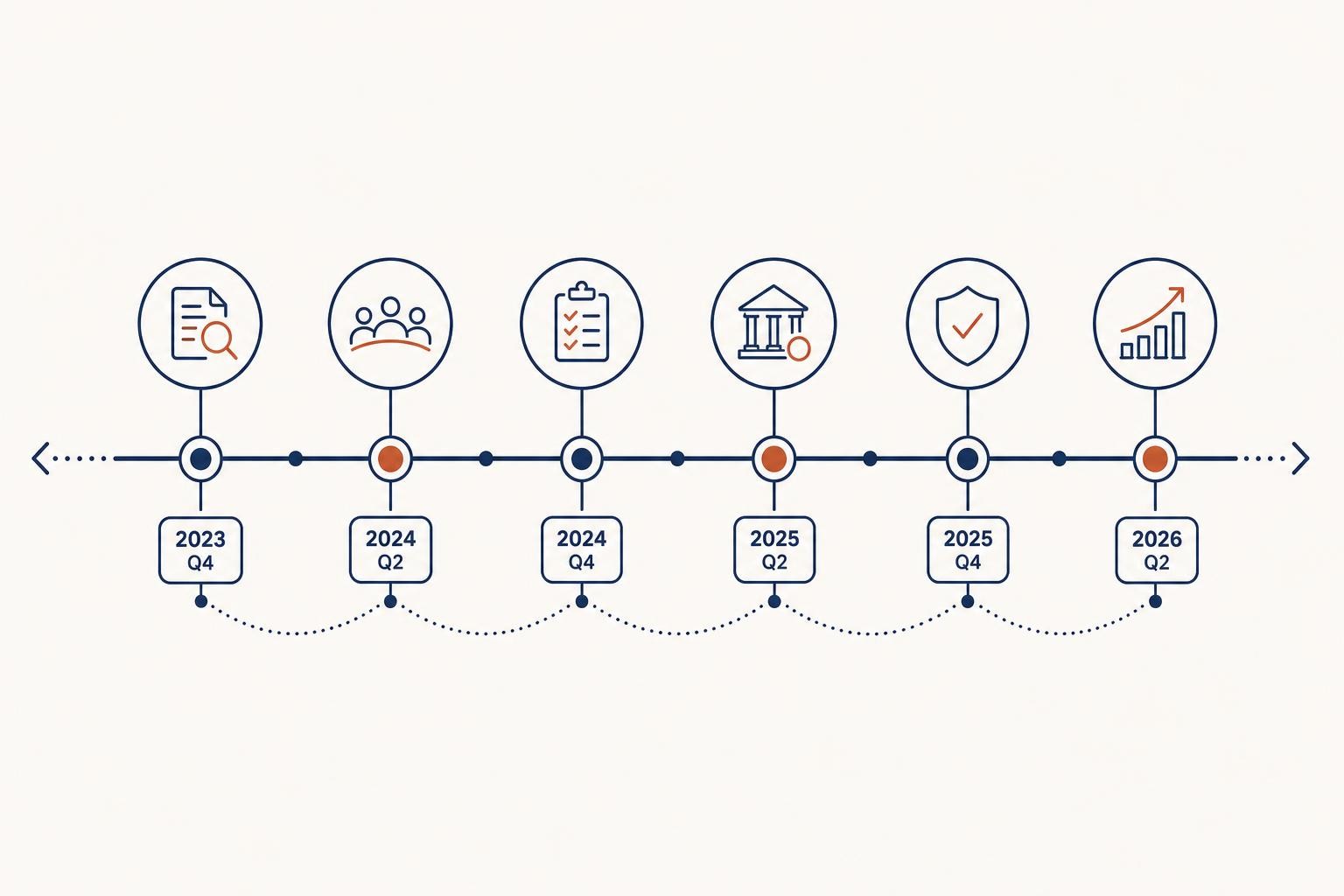

The 2026->2027 Retrospective Timeline

The Omnibus simplification (Regulation (EU) 2025/2083) restructured the entire first compliance cycle into a retrospective model. Here is what that means in practice:

Certificate sales via the EU's centralised common platform open on 1 February 2027, covering embedded emissions from goods imported during 2026. There is no obligation to hold certificates during 2026 itself - you are accumulating the liability, not yet paying it.

The annual CBAM declaration and certificate surrender deadline for 2026 imports is 30 September 2027. That is four months later than the original 31 May deadline, giving importers more time to finalise verified emissions data and acquire certificates.

The key implication: your entire 2026 CBAM liability crystallises in a seven-month window between 1 February and 30 September 2027. That is a concentrated cash-flow event - and the reason treasury teams need to start modelling it now, not in January 2027.

How the Certificate Price Is Set

CBAM certificate prices are not set by the market - they are calculated by the European Commission and published in the CBAM Registry.

For 2026 imports: Certificates are priced at the volume-weighted quarterly average of EU ETS allowance auction prices for each quarter of 2026. The Commission publishes each quarterly price within the first week after the quarter closes. The first price ever published was €75.36 per tonne CO₂e for Q1 2026, released on 7 April 2026.

From 2027 imports onward: The averaging period shortens to weekly. From 2027, the CBAM certificate price reflects the weekly average of EU ETS auction closing prices. This means prices will move more frequently and track the live carbon market more closely.

What this means for treasury: You cannot buy certificates at the live ETS spot price. You buy at the official published average. If ETS prices spike in February, your Q1 average will still partially reflect the lower January prices. That smoothing effect disappears from 2027, when weekly averaging kicks in - so price volatility becomes a more direct cash-flow risk for future years.

Watch the EU ETS price throughout 2026 even though you cannot buy certificates yet. Each quarter's average becomes the locked-in price for that tranche of your liability. A rising ETS price in Q3 or Q4 2026 will increase the cost of certificates you buy in 2027 for those imports. Monthly accruals based on the running quarterly average give your P&L an accurate picture before the bill arrives.

The 50% Quarterly Holding Rule - and Why It Matters

From 2027, the quarterly minimum holding rule applies. Here is the precise obligation:

At the end of each quarter (31 March, 30 June, 30 September, and 31 December), an authorised CBAM declarant must hold CBAM certificates equal to at least 50% of the embedded emissions of all goods imported since the start of that calendar year.

The Omnibus amendment reduced this from the originally planned 80% threshold. That reduction is meaningful: it cuts the working capital you need to tie up in certificates at each quarter-end checkpoint by more than a third compared to the original design.

The cumulative nature is the key detail. The 50% test is applied to all imports since 1 January, not just the most recent quarter. So by 30 September, you need certificates covering 50% of nine months of imports - not just Q3. Your certificate holdings must grow through the year.

A Worked Example: Accruing the Liability Through the Year

Suppose your company imports steel and aluminium with a total embedded emissions figure of 1,000 tCO₂e spread evenly across 2027 (250 tCO₂e per quarter). Assume a flat certificate price of €70/tonne for simplicity.

For a static illustration: an importer with 1,000 tCO₂e evenly spread across 2027 at €70/tonne would need to hold at least 125 certificates by end-Q1 (50% × 250 tCO₂e), 250 by end-Q2, 375 by end-Q3, and 500 by end-Q4 - then surrender all 1,000 by 30 September 2028. Buying only to the minimum each quarter means four separate purchases of 125 certificates each, costing €8,750 per tranche. Waiting until September to buy all 1,000 at once would breach the quarterly rules for Q1-Q3 and expose you to penalties.

The Surrender Deadline and What Happens After

By 30 September of the year following import, you must surrender the full number of certificates matching your verified embedded emissions (adjusted for any carbon price already paid in the country of origin, and for the EU ETS free allocation factor).

After surrender, if you hold surplus certificates - perhaps because your actual emissions came in below your quarterly purchases - you can request a repurchase. Repurchase requests must be submitted by 31 October of the year of surrender, and any certificates remaining in accounts on 1 November are cancelled by the Commission without compensation. Do not over-buy and miss the repurchase window.

The penalty for under-surrender is severe. Failing to surrender sufficient certificates carries a penalty of €100 per tonne of CO₂, indexed to the European consumer price index - and paying the fine does not extinguish the obligation to surrender the missing certificates. You pay both the penalty and the certificate cost.

Practical Treasury Tips

Five actions for your finance team right now:

- Accrue monthly. Book a CBAM liability each month based on that quarter's running EU ETS average price × your embedded emissions estimate. Don't wait for the annual declaration.

- Model four purchase tranches, not one. Plan certificate purchases at each quarter-end to meet the 50% minimum — spreading cost and reducing price-concentration risk.

- Watch the EU ETS price. For 2026 imports, each quarter's average is locked in at quarter-close. For 2027+ imports, weekly averages mean faster price pass-through.

- Don't over-buy without a plan. Surplus certificates can be repurchased, but only if you request it by 31 October. Miss that window and they are cancelled with no refund.

- Factor in the CBAM factor ramp. The free-allocation adjustment means only 2.5% of embedded emissions are payable in 2026, rising steeply toward 100% in 2034. Your 2026 cost is a fraction of your long-run exposure — model the full ramp in your multi-year budget.

The Cost Tracks the Carbon Price - Plan Accordingly

CBAM cost is not a fixed tariff. It moves with the EU ETS. The Q1 2026 price of €75.36/tCO₂e is a data point, not a forecast. ETS prices respond to policy signals, energy market conditions, and the pace of industrial decarbonisation across Europe.

For treasury purposes, the most useful approach is scenario planning: model a base case (current ETS price), a downside (ETS softens), and an upside (ETS tightens toward €90-100). The CBAM factor ramp means that even a flat ETS price produces a rising CBAM bill year-on-year through 2034, as the free-allocation adjustment phases out.

Key Dates at a Glance

| Event | Date | What to do |

|---|---|---|

| Definitive period begins; liability accrues | 1 Jan 2026 | Track imports and embedded emissions monthly |

| Q1 2026 certificate price published | ~7 Apr 2026 | Book Q1 CBAM accrual at €75.36/tCO₂e |

| Q2 2026 certificate price published | ~7 Jul 2026 | Update accrual for Q2 imports |

| Q3 2026 certificate price published | ~7 Oct 2026 | Update accrual for Q3 imports |

| Q4 2026 certificate price published | ~7 Jan 2027 | Finalise full-year liability estimate |

| Certificate sales open (centralised platform) | 1 Feb 2027 | Begin purchasing certificates; plan four quarterly tranches |

| Q1 2027 quarterly holding check (50% of YTD imports) | 31 Mar 2027 | Ensure account holds ≥50% of cumulative 2027 embedded emissions |

| Q2 2027 quarterly holding check | 30 Jun 2027 | Top up holdings to ≥50% of H1 2027 cumulative emissions |

| Annual declaration + surrender deadline (2026 imports) | 30 Sep 2027 | Submit declaration; surrender full certificate amount for 2026 |

| Q3 2027 quarterly holding check | 30 Sep 2027 | Also meet 50% holding for 2027 YTD imports on same date |

| Repurchase request deadline (surplus 2026 certificates) | 31 Oct 2027 | Request repurchase of any surplus certificates |

| Unsurrendered 2026 certificates cancelled | 1 Nov 2027 | No action possible after this date — plan ahead |

The certificate mechanics are now clear. The harder work is building the internal processes - monthly accruals, quarterly purchase plans, supplier data pipelines - that make compliance feel routine rather than a crisis. Start that work now, while 2026 is still the year you are building the liability, not the year you are paying it.

Related reading

The Article 9 Deduction: How to Cut Your CBAM Certificate Bill with Carbon Prices Paid Abroad

Article 9 of Regulation (EU) 2023/956 lets you deduct a carbon price already paid in the country of origin from your CBAM certificate obligation. Here's exactly how it works - and how to claim it.

CBAM Record-Keeping and Audit Readiness: The Importer's Practical Guide

CBAM compliance isn't just about the 30 September declaration. Here's the practical guide to the data trail, four-year retention rules, and NCA audit readiness every authorised declarant needs.

CBAM and Imported Electricity: Why the Physical Hourly PPA Is Now the Only Route Off the Default

Electricity behaves differently under CBAM than any other covered sector. Here's exactly how the definitive regime works for cross-border power - and why only a physical hourly PPA can reduce your liability.