How to File Your First Annual CBAM Declaration: A Practical Guide to the 30 September 2027 Deadline

The quarterly CBAM reports you filed during the transitional period (2023-2025) are over. What comes next is different in almost every way: it's annual, it carries real financial consequences, and it ends with you surrendering CBAM certificates worth real money. The first annual CBAM declaration covers all CBAM goods you imported during 2026, and it is due 30 September 2027.

This guide is specifically about filing that declaration - not about applying for authorised declarant status (we cover that separately). If you already hold authorised declarant status and are asking "what do I actually submit, and when?", read on.

The Deadline Change You Need to Know

The original CBAM Regulation set the annual declaration deadline at 31 May each year, with the first due 31 May 2027. The Omnibus simplification package changed that.

The Omnibus amending act (Regulation (EU) 2025/2083) was published in the Official Journal on 17 October 2025 and entered into force on 20 October 2025. Among its most practically important changes: the deadline for the annual CBAM declaration and certificate surrender moved from 31 May to 30 September of the following year, giving importers an additional four months. That means the first annual CBAM declaration - covering goods imported during 2026 - is now due 30 September 2027.

The same deadline applies to certificate surrender. You declare and surrender on the same date.

Why does the extra time matter? Verification of actual embedded emissions takes time. Suppliers need to compile installation-level data; accredited verifiers need to review it. Four extra months makes the difference between a rushed, default-value declaration and one based on verified actual emissions - which typically means a lower certificate bill.

Who Must File - and Who Is Exempt

Before diving into the mechanics, confirm whether you are required to file at all.

The 50-tonne de minimis threshold

The Omnibus simplification replaced the old €150-per-consignment trigger with a single mass-based threshold: importers bringing in 50 tonnes or less (cumulative net mass) of CBAM-covered goods per calendar year are exempt from all CBAM obligations - no declaration, no authorisation, no certificates. The threshold is measured per legal entity (EORI number) across the full calendar year, aggregating all covered goods.

Hydrogen and electricity are excluded from this de minimis exemption - they are subject to CBAM obligations regardless of volume.

One important catch: if an importer exceeds the 50-tonne threshold at any point during the year, all imports for that year become subject to CBAM obligations. There is no partial exemption for the portion below 50 tonnes.

The 50-tonne threshold is an annual aggregate, not a per-shipment test. If you import 30 tonnes of steel in Q1 and 25 tonnes of aluminium in Q3, you have crossed 55 tonnes combined and CBAM applies to your entire year's imports — retroactively from 1 January.

Only authorised declarants can file

Only authorised CBAM declarants may import CBAM goods above the threshold and submit the annual declaration via the definitive CBAM Registry. If you are still awaiting authorisation, you cannot file. Confirm your status with your National Competent Authority (NCA) well before the declaration window opens.

What the Annual Declaration Contains

The annual declaration is not a narrative report - it is a structured submission in the CBAM Registry. At its core, it must include:

- The quantity of CBAM goods imported during the calendar year, broken down by CN code and country of origin.

- The total embedded emissions associated with those goods - either actual verified values or EU default values.

- The number of CBAM certificates to be surrendered, after deducting any carbon price already effectively paid in the country of origin, and after the free allocation adjustment.

EU importers must declare the emissions embedded in their imports and surrender the corresponding number of CBAM certificates each year; if importers can prove that a carbon price has already been paid during the production of the imported goods, the corresponding amount can be deducted.

Each CBAM certificate represents one tonne of CO₂ equivalent of embedded emissions. The number you surrender equals your total declared embedded emissions, minus the free allocation adjustment (which reflects the phasing-out of free EU ETS allowances for domestic producers), minus any verified carbon price paid abroad.

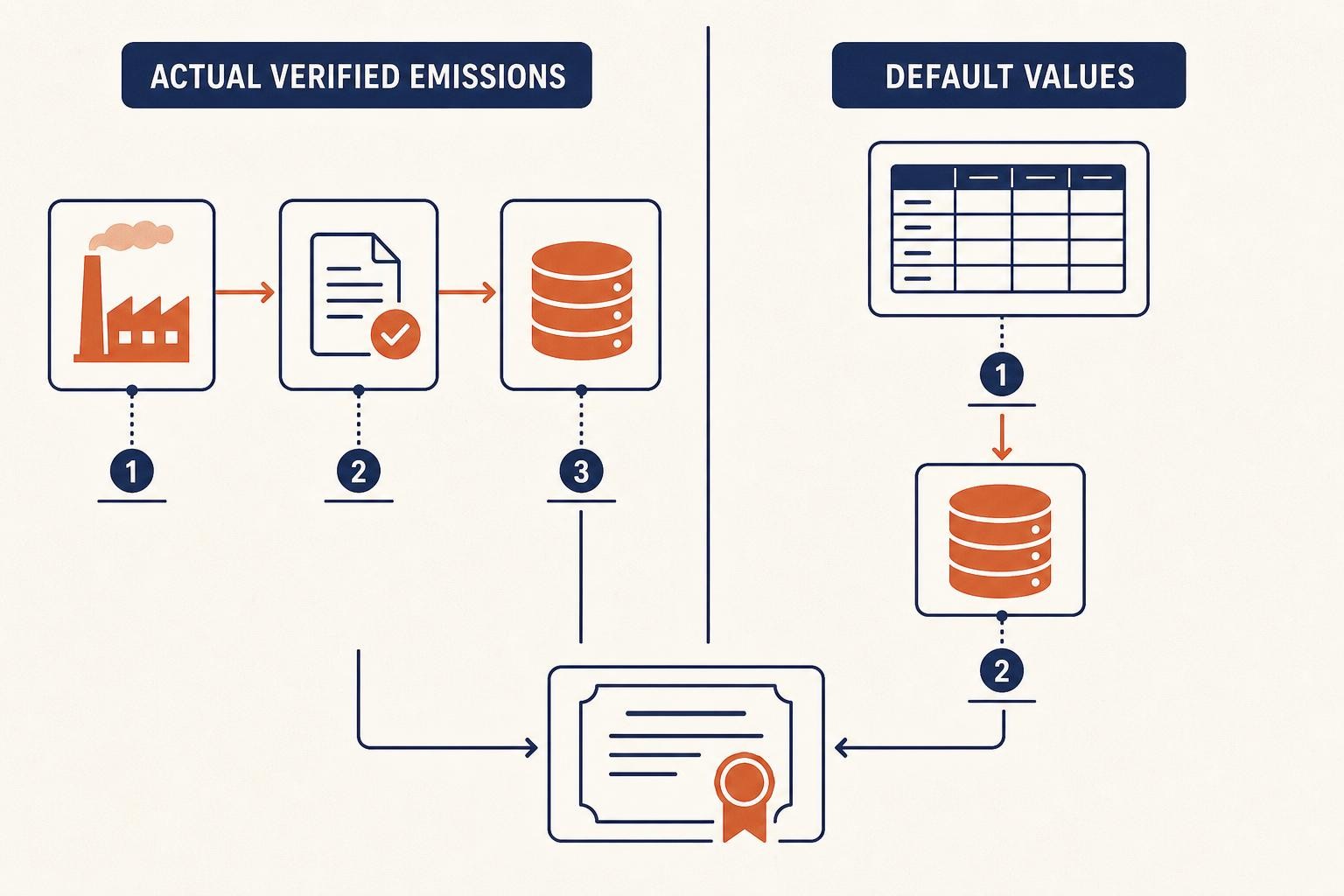

Actual values vs default values

You have a choice for how to calculate embedded emissions:

- Actual verified values: Installation-level data from your non-EU supplier, verified by an EU-accredited third-party verifier. Verification by an accredited verifier is required only when using actual values - not when using default values. Actual values typically produce a lower certificate obligation if your supplier's production is cleaner than the default.

- Default values: Published by the Commission in Implementing Regulation (EU) 2025/2621. These are intentionally conservative - default values carry a mark-up of 10% above the calculated default in 2026, rising to 20% in 2027 and 30% from 2028 onwards (with a flat 1% mark-up for fertilisers). Using defaults is simpler but usually more expensive.

The Certificate Timeline: How Quarterly Holdings Relate to the Annual Declaration

This is where many importers get confused. There are two separate but linked obligations:

1. Quarterly certificate-holding requirement (from Q1 2027)

CBAM certificate sales start on 1 February 2027. From that point, you must hold a minimum number of certificates in your CBAM Registry account at the end of each quarter. The quarterly holding requirement is 50% of the cumulative embedded emissions of CBAM goods imported since the start of the calendar year - reduced from the original 80% by the Omnibus simplification.

This is assessed at the end of each quarter (31 March, 30 June, 30 September, 31 December). It is a holding obligation - you are not surrendering certificates quarterly, just demonstrating you hold enough to cover half your year-to-date exposure.

2. Annual declaration and full surrender (30 September 2027)

The annual declaration is where you declare your total 2026 embedded emissions and surrender the full corresponding number of certificates. The quarterly holdings you built up during 2027 count toward this final surrender.

The key distinction: quarterly holdings are a liquidity check; the annual declaration is the final reckoning. You cannot substitute quarterly reports for the annual declaration - they serve different purposes.

Step-by-Step: Preparing and Filing the Declaration

Log into the CBAM Registry (the definitive registry, not the transitional one) and verify your authorisation is active and your account is in good standing. If your NCA has not yet issued a decision, chase it now — you cannot file without it. Check that your EORI number is correctly linked.

Pull your customs import records for the full calendar year 2026. Aggregate the net mass of all CBAM-covered goods (cement, iron & steel, aluminium, fertilisers, hydrogen, electricity) imported under your EORI number. If the total is 50 tonnes or less (and you import no electricity or hydrogen), you are exempt and do not need to file. If you exceed it, proceed.

For each installation supplying CBAM goods, you need either: (a) a verified emissions report from an EU-accredited verifier covering the 2026 production period, or (b) the applicable EU default values from IR (EU) 2025/2621. Request supplier data early — verification takes time, and verifiers will be busy ahead of the September 2027 deadline. Non-EU operators can upload their installation data directly to the CBAM Registry for sharing with declarants.

Multiply the quantity of each imported good (in tonnes) by its specific embedded emissions (tCO₂e per tonne). Sum across all goods and installations. Then apply the free allocation adjustment — this reduces your certificate obligation to reflect the free EU ETS allowances still granted to domestic EU producers. The calculation rules are set out in IR (EU) 2025/2620.

If a carbon price was effectively paid in the country of origin (or in any third country in the production chain), you may deduct the corresponding amount from your certificate obligation. From 2027, the Commission publishes default carbon prices for countries with carbon pricing mechanisms in the CBAM Registry. Gather evidence of actual payments if you intend to claim a deduction.

Certificates are sold by your national authority via the EU central platform, starting 1 February 2027. For 2026 imports, the certificate price is based on the quarterly average of EU ETS auction clearing prices during the quarter of importation — not the price at the time of purchase. Keep records of which goods were imported in which quarter, as this determines the applicable price.

Log into the definitive CBAM Registry and complete the annual declaration form. You will enter: quantities by CN code and country of origin; embedded emissions per good (actual or default); the free allocation adjustment; any carbon price deductions; and the number of certificates to be surrendered. The Registry does not calculate these figures for you — arrive with your numbers ready.

Select the certificates in your CBAM Registry account that you wish to surrender. The number surrendered must equal the total embedded emissions declared, after all adjustments and deductions. This step and the declaration submission happen together — both are due by 30 September 2027.

The Regulatory Framework Behind the Declaration

The rules governing the annual declaration are now settled across two waves of legislation:

Regulation (EU) 2025/2083 (the Omnibus amending act): published in the Official Journal on 17 October 2025, it moved the annual declaration deadline to 30 September, reduced the quarterly holding requirement from 80% to 50%, and introduced the 50-tonne mass-based de minimis threshold.

The December 2025 implementing package: on 17 December 2025, the European Commission published a package of implementing and delegated acts to make CBAM fully operational for the definitive phase starting 1 January 2026. This package covers the emissions calculation methodology (IR 2025/2547), default values (IR 2025/2621), the free allocation adjustment (IR 2025/2620), certificate pricing (IR 2025/2548), the definitive CBAM Registry rules, and verifier accreditation (DR 2025/2551).

Together, these acts give you the complete technical rulebook for your first declaration. The EU Taxation & Customs CBAM Registry and Reporting page is the authoritative source for Registry access and user guidance.

What Happens If You Miss the Deadline or Under-Surrender?

The penalty regime in the definitive phase is serious. The penalty for failing to surrender the required number of certificates mirrors the EU ETS excess emissions penalty of €100 per tonne of CO₂, and importers who import CBAM goods without authorisation may face penalties up to five times that amount. Paying the penalty does not extinguish the obligation to surrender the outstanding certificates.

Customs authorities will implement CBAM controls through the EU Customs Single Window, resulting in automated compliance checks at the border - imports not declared by an authorised CBAM declarant will be refused customs clearance.

Your 2026 Action Checklist

You have until 30 September 2027 to file, but the data you need is being created right now, throughout 2026. Waiting until mid-2027 to start collecting it is the most common mistake.

Here is a plain-text summary of the key dates to track:

| Date | What happens |

|---|---|

| Throughout 2026 | Collect supplier emissions data; track import volumes against 50-tonne threshold |

| 1 February 2027 | CBAM certificate sales open |

| 31 March 2027 | Q1 2027 quarterly holding check (≥50% of year-to-date embedded emissions) |

| 30 June 2027 | Q2 2027 quarterly holding check |

| 30 September 2027 | Annual declaration due + full certificate surrender for 2026 imports |

| 31 October 2027 | Deadline for certificate repurchase requests |

Practical Tips Before You File

Start supplier conversations now. Verification of actual emissions takes months. If your supplier has not yet engaged an accredited verifier, the September 2027 deadline will arrive before the verification report does - leaving you reliant on default values and a higher certificate bill.

Track quarterly imports, not just annual totals. For 2026 imports, the certificate price is based on the quarter in which the goods were imported (not the quarter in which you buy the certificates in 2027). Keep a record of import dates and volumes by quarter throughout 2026.

Default values are a fallback, not a strategy. The mark-up on default values (10% in 2026, rising to 30% from 2028) means that importers who invest in actual verified data will consistently pay less. The gap widens every year.

Delegation is allowed, but liability stays with you. Authorised CBAM declarants may delegate the filing of CBAM declarations to EU-established third parties holding an EORI number, but remain responsible for compliance. If you use a customs broker or representative, ensure they have the data they need and that you have reviewed the declaration before submission.

Keep records for four years. The CBAM Regulation requires you to retain the information used to calculate embedded emissions for at least four years. Treat your declaration data with the same rigour as a financial audit.

The 30 September 2027 deadline is further away than the original May date, but the data collection work starts now. The importers who will file smoothly are the ones building their emissions data workflows in 2026 - not the ones scrambling in August 2027.

Related reading

Steel's 2026 Double Squeeze: CBAM Goes Live and the Safeguard Gets Tougher

From 1 January 2026 CBAM is financially binding. From 1 July 2026 a tougher steel safeguard halves quota volumes and doubles the out-of-quota tariff to 50%. Here's what both mean for steel importers and exporters.

CBAM Cost Trajectory: Why 2026 Is Cheap and 2030 Will Hurt

CBAM looks affordable in 2026 - but the cost escalates nearly 40x by 2034. Here's the full phase-in schedule, the 2029-2030 cliff edge, and how to budget now.

CBAM Penalties and Enforcement: What EU Importers Need to Know

A clear guide to CBAM penalties under the definitive regime - the €100/tonne rule, unauthorised-import sanctions, how member states enforce, and how to stay on the right side of the rules.